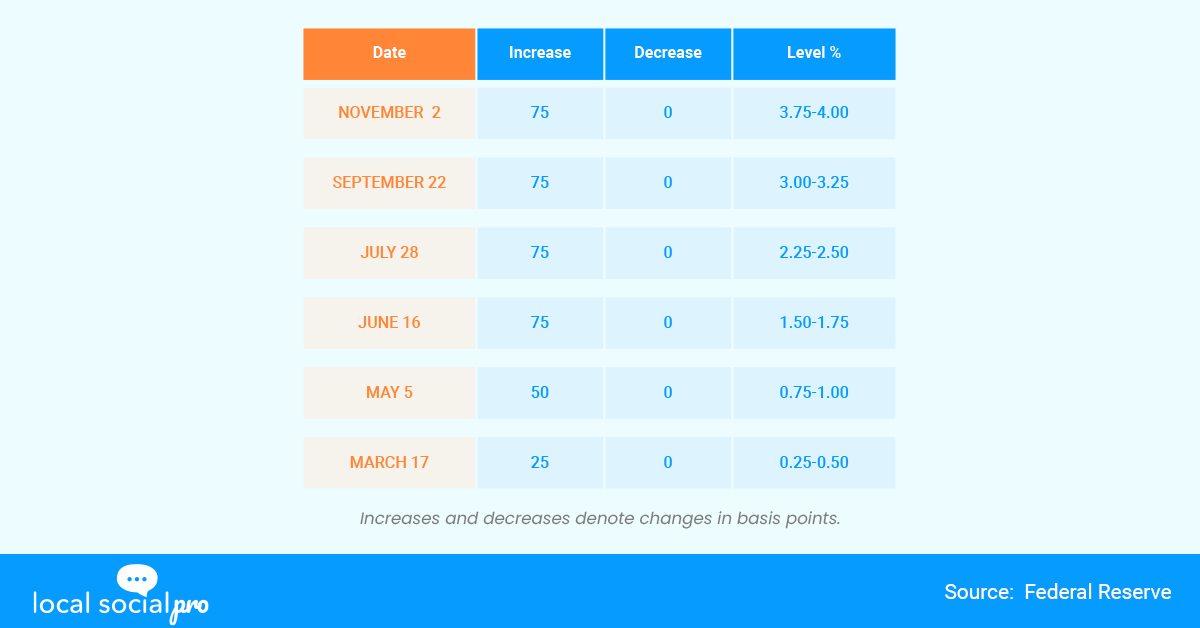

The Federal Reserve announced a fourth consecutive three-quarter point hike in interest rates, signaling a possible shift in how it will handle monetary policy to reduce inflation. Even as households of all income levels feel past rate increases, it was the Fed’s sixth rate hike of the year. The central bank boosted its narrow loan rates by 0.75 percentage points to 3.75%-4%, the highest since January 2008. Another hike is scheduled before the end of the year, and the central bank has promised to keep rates high until inflation returns to normal levels. The Fed’s most recent action increased its benchmark rate from 3.75% to 4%, the highest point in 14 years. Its continuous rate rises have already made borrowing for homes, cars, and other purchases more expensive for families and businesses. And additional raises are virtually certainly on the way.

Grote Winnaars en Succesverhalen in Nederlandse Online Casino’s

Welkom bij ons artikel over de grote winnaars en succesverhalen in Nederlandse online casino’s! Het online gokken heeft de afgelopen jaren een enorme populariteit gekend, en steeds meer spelers in Nederland wagen hun kans in de virtuele wereld van casino spellen. Maar wie zijn de gelukkige winnaars die erin slagen om grote bedragen te winnen? En wat zijn de succesverhalen die ons inspireren en laten zien dat het mogelijk is om een fortuin te vergaren met online gokken?

In dit artikel zullen we enkele van de meest opmerkelijke winnaars en succesverhalen uit Nederlandse online casino’s onder de loep nemen. We zullen je meenemen op een spannende reis door de wereld van online gokken, waar we de verhalen van spelers ontdekken die hun leven hebben veranderd door een enkele draai aan het roulettewiel of een gelukkige combinatie op de gokkast. Bereid je voor om geïnspireerd te worden door ongelooflijke overwinningen en te leren van de strategieën en tips van degenen die het geluk aan hun zijde hadden. Ben jij klaar om te ontdekken wat er mogelijk is in de wereld van Nederlandse online casino’s? Lees dan snel verder!

Opkomst van Nederlandse online casino’s: Een overzicht van de belangrijkste spelers in de markt

Online casino’s zijn de afgelopen jaren enorm populair geworden in Nederland, en er zijn al veel grote winnaars en succesverhalen te vinden. Een van de meest opvallende is het verhaal van Jan uit Amsterdam. Hij besloot om een gokje te wagen bij een bekend online casino en won maar liefst €100.000 met een enkele draai aan de gokkast. Jan was compleet verrast en kon zijn geluk niet op. Hij gebruikte zijn winst om zijn droomreis naar de Cariben te maken en een nieuwe auto te kopen. Dit succesverhaal inspireert veel andere spelers om ook hun geluk te beproeven in Nederlandse online casino’s.

Een ander indrukwekkend succesverhaal komt van Linda uit Utrecht. Na een lange dag werken, besloot ze om haar favoriete online casino te bezoeken en een paar rondes blackjack te spelen. Tot haar verbazing won ze opeenvolgend verschillende grote prijzen en eindigde de avond met een totale winst van €50.000. Linda was dolgelukkig en gebruikte het geld om haar studielening af te betalen en een deel te investeren in haar eigen bedrijf. Haar verhaal laat zien dat het spelen in Nederlandse online casino’s niet alleen leuk is, maar ook kan leiden tot grote financiële successen.

Miljoenenjackpots: De grootste winnaars in Nederlandse online casino’s

Grote Winnaars en Succesverhalen in Nederlandse Online Casino’s zijn een bron van opwinding en inspiratie voor spelers overal ter wereld. Casizoid Netherlands, een van de meest populaire online casino’s in Nederland, heeft al vele indrukwekkende winnaars voortgebracht. Van enorme jackpots tot spannende toernooioverwinningen, Casizoid Netherlands heeft een reputatie opgebouwd als een platform waar geluk en succes samenkomen.

Een van de meest opmerkelijke succesverhalen bij Casizoid Netherlands is dat van Lisa Jansen. Ze speelde regelmatig op het online casino en had nooit gedacht dat ze ooit een grote winnaar zou worden. Maar op een gelukkige dag draaide ze aan de rollen van een videoslot en won ze een ongelooflijke jackpot van €100.000! Lisa kon haar geluk niet geloven en het geld kwam precies op het juiste moment. Ze besloot een deel van haar winst te investeren in haar droomreis naar de Cariben en de rest te sparen voor de toekomst.

Succesvolle strategieën: Hoe sommige spelers consistent winnen in online casino’s

De wereld van online casino’s in Nederland heeft de afgelopen jaren een enorme groei doorgemaakt, en dit heeft geleid tot enkele grote winnaars en succesverhalen. Een van de meest opmerkelijke verhalen is dat van een speler die onlangs een enorm bedrag heeft gewonnen bij een bekend Nederlands online casino. Met slechts een kleine inzet slaagde deze gelukkige speler erin om een jackpot van maar liefst €1 miljoen te winnen. Dit winnende bedrag heeft zijn leven voorgoed veranderd en is een inspiratie voor vele andere spelers die dromen van grote overwinningen.

Een ander succesverhaal komt van een Nederlandse vrouw die haar geluk beproefde bij een online gokkast en een aanzienlijk bedrag wist te winnen. Met haar winst kon ze haar droomreis maken naar een exotische bestemming waar ze altijd al van had gedroomd. Deze overwinning heeft haar niet alleen financiële vrijheid gegeven, maar ook de mogelijkheid om haar leven op een geheel nieuwe manier vorm te geven. Dit is slechts een van de vele succesverhalen van spelers die hun geluk hebben gevonden in de Nederlandse online casino’s.

Innovatie en technologie: Hoe Nederlandse online casino’s zich onderscheiden in de industrie

De wereld van online casino’s in Nederland heeft de afgelopen jaren een enorme groei doorgemaakt. Met de legalisatie van online gokken in 2021 zijn er talloze nieuwe spelers op de markt gekomen. Enkele van de grote winnaars en succesverhalen in Nederlandse online casino’s zijn echter al langer actief en hebben een indrukwekkend trackrecord opgebouwd.

Eén van de meest opvallende succesverhalen is dat van een speler die in 2015 bij een Nederlands online casino maar liefst €1,9 miljoen won. Deze gelukkige winnaar speelde op een progressieve jackpot gokkast en zag zijn leven in één klap veranderen. Met dit enorme bedrag kon hij zijn dromen verwezenlijken en genieten van een leven vol luxe en comfort.

Een ander indrukwekkend succesverhaal komt van een Nederlandse speler die in 2019 een gigantische jackpot van €3,7 miljoen won bij een online casino. Deze winnaar speelde op een videoslot en had nooit durven dromen van zo’n grote prijs. Met het gewonnen geld heeft hij zijn huis kunnen afbetalen, zijn familie financieel kunnen ondersteunen en de reis van zijn leven kunnen maken.

Tot slot is er het verhaal van een Nederlandse vrouw die in 2020 een bedrag van €1,2 miljoen won bij een online casino. Deze winst kwam na een paar uur spelen op verschillende gokkasten. Ze was compleet verrast en kon haar geluk niet op. Met het gewonnen geld heeft ze haar schulden afbetaald en haar droomreis kunnen maken naar de Seychellen.

Regulering en veiligheid: Het belang van een betrouwbare en verantwoorde online casino-ervaring in Nederland

In Nederlandse online casino’s zijn er talloze grote winnaars en succesverhalen te vinden. Een van de meest opmerkelijke verhalen is dat van een gelukkige speler die een miljoenenjackpot won op een gokautomaat. Met slechts een kleine inzet veranderde deze speler zijn leven voorgoed. Dit soort grote winsten zijn niet ongewoon in de wereld van online gokken, waar geluk en strategie samenkomen.

Een ander succesverhaal is dat van een professionele pokerspeler die zijn vaardigheden online heeft ingezet en grote successen heeft behaald. Met zijn strategisch inzicht en ervaring heeft hij meerdere grote pokertoernooien gewonnen en aanzienlijke geldprijzen in de wacht gesleept. Dit bewijst dat online casino’s niet alleen geluksspellen zijn, maar ook een plek waar talent en vaardigheid kunnen leiden tot indrukwekkende successen.

Al met al zijn er talloze grote winnaars en succesverhalen te vinden in Nederlandse online casino’s. Van spelers die met een kleine inzet een enorme jackpot winnen tot degenen die strategisch spelen en regelmatig mooie prijzen in de wacht slepen. Het is duidelijk dat online casino’s een opwindende en lonende ervaring kunnen bieden voor spelers van alle niveaus. Of je nu een ervaren gokker bent of net begint, de mogelijkheden zijn eindeloos. Dus waar wacht je nog op? Waag vandaag nog je kans en wie weet ben jij de volgende grote winnaar in een Nederlands online casino!

How does it Affect the Monetary Sector?

Modifications in the federal funds rate have an impact on both domestic and international markets. Bond dealers, Wall Street bankers, and market analysts are all attempting to forecast the Fed’s next moves. This enhances the impact of interest rate hikes and central bank communications. Analysts may examine Fed speeches in the hopes of deriving any signals on the precise scale of the upcoming interest rate hike, allowing markets to begin pricing in any moves ahead of time. Changes in the Fed’s overnight rate also have an impact on the value of various financial instruments.

Which Consumers are Significantly Affected?

According to Scott Hoyt, an analyst with Moody’s Analytics, anyone borrowing money to make a significant purchase, such as a home, car, or large equipment, will take an impact.

“The new rate pretty dramatically increases your monthly payments and your cost… It also affects consumers who have a lot of credit card debt — that will hit right away.”

– Scott Hoyt, Moody’s Analytics analyst

Hoyt did observe, however, that family debt payments as a percentage of income remain relatively modest, notwithstanding recent increases. As a result, even as borrowing rates continuously rise, many households may not instantly feel a significantly larger debt load.

“I’m not sure interest rates are top of mind for most consumers right now… They seem more worried about groceries and what’s going on at the gas pump. Rates can be something tricky for consumers to wrap their minds around.”

– Scott Hoyt, Moody’s Analytics analyst

In regards to the effect on credit cards, when the economy is facing a significant slowdown or inflation is increasing rise, they may increase or drop this rate in order to boost or reduce the cost of borrowing. This will also have an impact on the prime rate, which refers to the interest rate that banks charge their core customers. This rate is also used by credit card companies to calculate your APR, which, according to Federal Reserve data, will average 16.65% in the second quarter of 2022, while certain cards may have interest rates of more than 20%. These actions will eventually have an effect on you as a consumer. As a result, when the Fed boosts this rate, you’re likely to notice a few modifications in credit-card terms.

The Bottom Line:

Don’t be caught off guard by the Fed’s initiatives. Knowing when it may raise or lower interest rates can help you make more educated decisions about your own finances and come out ahead even if rates remain unchanged. It’s better to keep in touch with your local expert and figure out the best way to navigate through this ever-changing market.

What To Do:

Did you find this read interesting? Need expert and white glove advice? Get in touch for local and professional real estate advice in your neighborhood. Fill in the form above to speak with a real estate professional that specializes in this topic and more!